#11 WTF are debt instruments? - Part 1

Read Time: 16 minutes

7,600+ curious folks read Simplanations. Join them by signing up here:

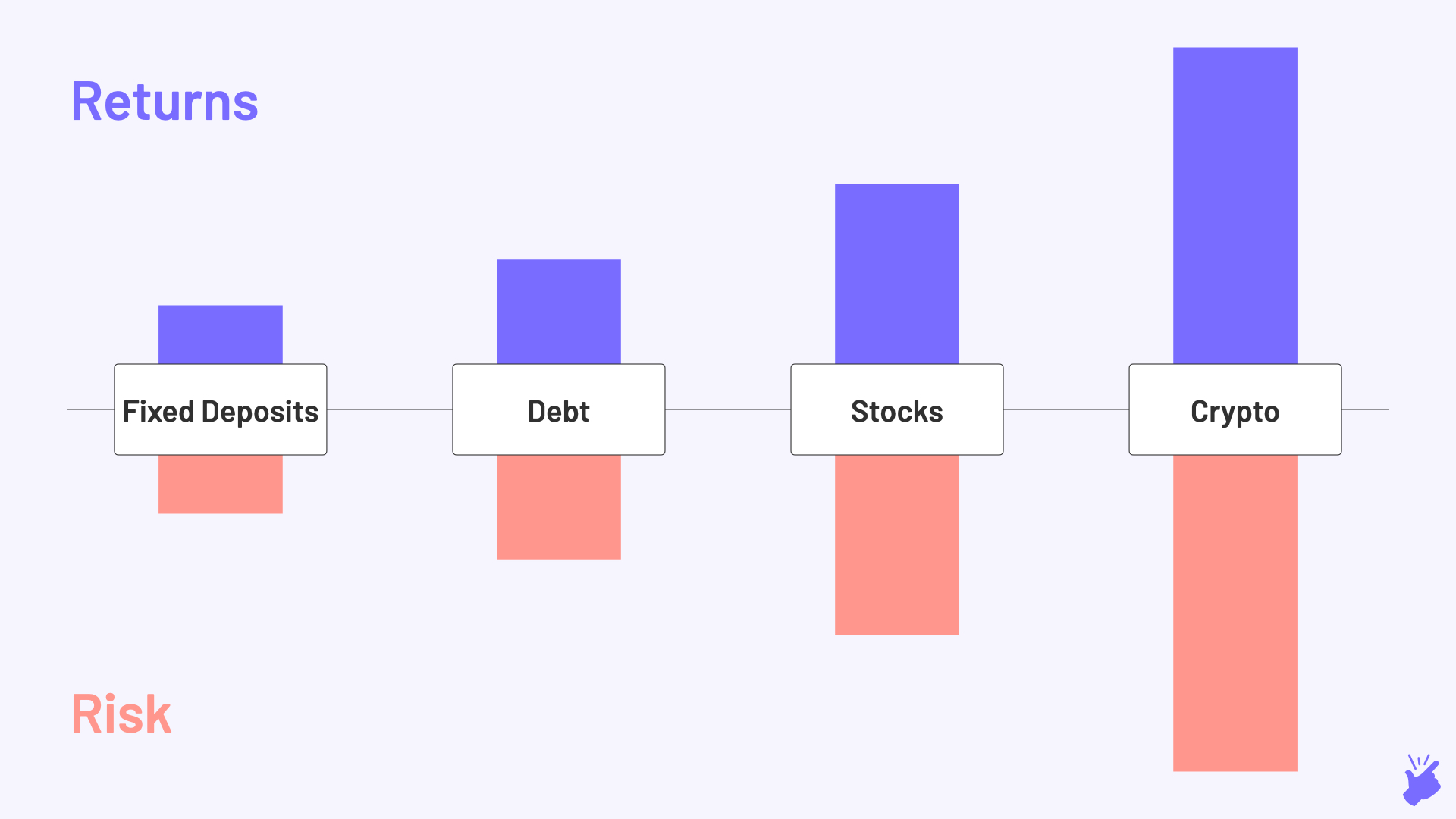

Over the past few decades, there have been quite a lot of changes in the way people invest. A couple of decades ago, people preferred to invest only in bank deposits which offered low but safe returns. In the late 2000s, more investors started pouring money into equity mutual funds and stocks. These did offer much higher returns but were prone to high fluctuations if the market or a stock crashes. Also, the timing of investment in equity markets can have a huge impact on the returns generated. In the past few years, cryptocurrency has been the buzzword. These novel investments can offer unimaginable returns but they can be extremely volatile. And finally, the latest trend in the form of NFTs when people decided to buy flying cat memes for 600,000 USD.

In the midst of all these publicly discussed options, people generally tend to miss out on another option: Debt instruments. These instruments typically offer a little higher return (8-10% per annum) than bank fixed deposits and are considered safer than equity and of course crypto.

In today’s post, we will try to simplain how debt instruments work.

So, what exactly are debt instruments?

All organizations like government bodies, PSUs, banks, infrastructure finance companies, regular corporates and Non-Banking Financial Companies (NBFCs) need capital to finance new projects and operations. To raise this new capital, companies issue debt instruments called bonds.

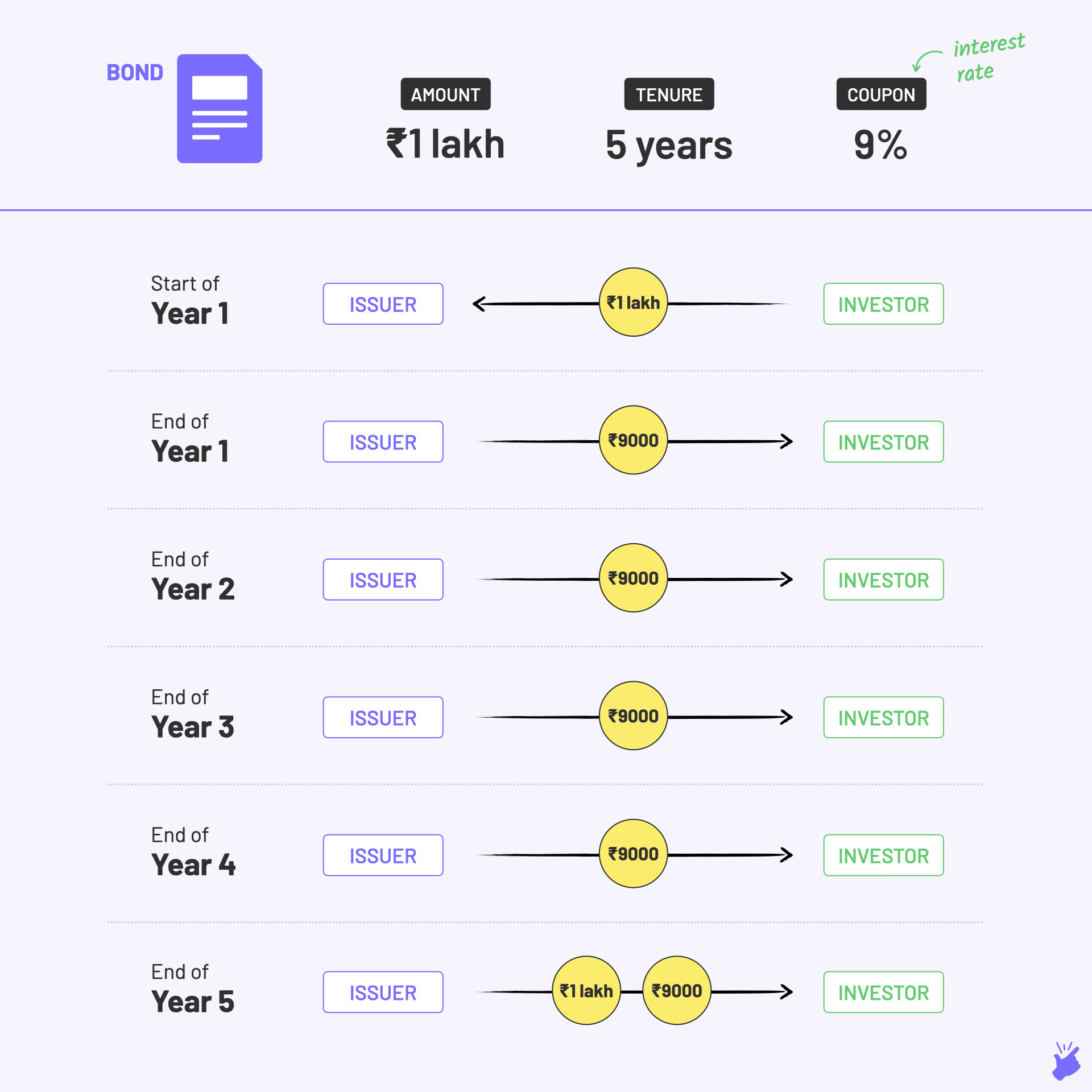

A bond is a financial instrument that represents a loan made by an investor to a borrower (government or corporate body in this case). Think of it as a document that includes all the details of the loan and the payments to be done. So, assume a company named ‘Repro Home Finance Limited (RHFL)’ wants to raise 10 crore INR from investors via bonds. It decides to issue 1000 bonds worth 1 lac INR each for a duration of 5 years with a coupon rate of 9%. Don’t worry about the terms for now; we will come to them later. If an investor likes this opportunity, he/she can become a bond holder by investing a minimum of 1 lac INR or its multiples for one or more units of the bond on offer.

Now after the bond holder has provided the loan to the bond issuer, let’s see how the repayment is done. The coupon rate is the interest rate paid by the bond issuer to the holder every year for the entire duration. So for 1 lac INR investment at a 9% coupon rate for a period of 5 years, bond holders get paid the interest amount: 9000 INR in this case at the end of every year for the entire duration: 5 years in this case. And at the end of the bond duration, they also get paid the principal which was 1 lac in this case. So ideally, a bond is a loan that an investor gives to the bond issuing organization with pre-defined payouts throughout the duration of the bond.

Below is a snapshot of some bonds available for purchase online. There are two things in the image that should catch your attention.

One - The minimum investment mentioned for all these bonds is around 10 lacs INR which is pretty high for a retail investor. In fact, over 90% of the bonds issued in India have such high ticket sizes and hence see minimal participation from small retail investors, ie, common investors like you and me.

Two - You’d have seen a term called “yield”. For now, let’s assume it’s the same as the coupon rate (interest rate). There is actually a nuanced difference between the two but I will explain that in detail later.

But why do companies need to “raise debt”, ie, “issue bonds”? Don’t they have other ways of arranging for money?

Valid question. Companies do have other alternatives - like take a bank loan or raise money from an initial public offering (IPO). Let’s look at each of these alternatives one by one.

Large organizations typically need more money than an average bank can provide. Also, extremely large bank loans come with a lot of terms & conditions as well as collateral - the security you give to a bank (like a house or vehicle) when you take a loan. Finally, the interest rates on bank loans tend to be higher than what companies need to pay when they raise by issuing bonds.

A lot of companies raise money through IPOs i.e. by selling their ownership in the company in return for funds from investors. But not every company might want to dilute its ownership every time it needs money. Also, government organizations like municipalities might not be suited to be listed on a stock exchange as they are not traditional business entities looking to maximize profits. Finally, NBFCs whose business model is to raise money and lend them out as loans cannot sell their stake every time they want to raise more capital.

Therefore, debt offers an effective means for companies to raise funds at a cheaper interest rate than bank loans without diluting their ownership.

Understood. But what happens if a company is unable to repay the money they got by issuing bonds?

When a bank gives out a loan it asks for some security called “collateral”. Even NBFCs that give personal, vehicle and home loans require security or a claim on the asset for which the loan is being given. For example, gold loan companies like Muthoot and Manappuram take gold as collateral from customers for the loans issued. On average these companies have an LTV (Loan To collateral Value) of 60-70% which means if a customer pledges gold worth 100 INR, then a loan of max 60-70 INR can be disbursed to the customer. This allows the NBFC to extract the money from the collateral if the customer defaults without incurring losses.

In a similar way, when bond investors loan to companies via bonds, they also get a claim to certain collateral against the loan. For most companies, it’s a pool of assets (like factories, machinery, office buildings, etc) on their balance sheet. And in the case of financial companies like, say an NBFC, the loans that the NBFC has given out are provided as collateral (loans given out by an NBFC are assets on its balance sheet since they generate regular income in form of loan repayments).

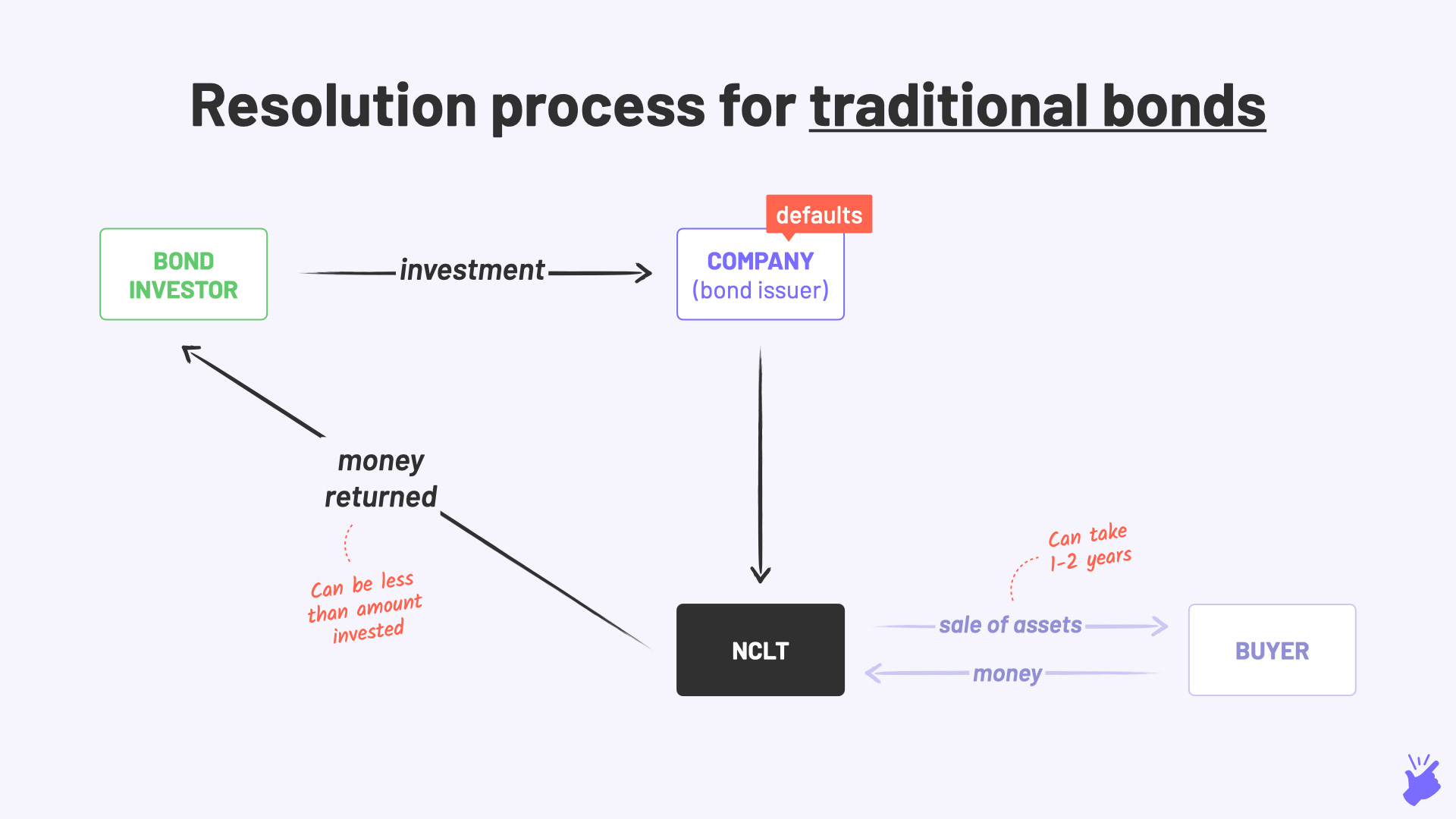

So when a company defaults (does not pay) on its bond payments, the assets (“collateral”) are sold (“liquidated”) and the money is paid to the investors. The process is painstakingly long and involves court proceedings.

This brings us to another question.

What if the defaulting company does not have enough assets on its balance sheet to pay back the bonds?

Then it's highly likely that the bond holders would not receive their complete investment. This risk of not getting back the entire money you lent via bonds is called credit risk. However, there is a process bond investors can follow to maximize the amount of money they can recover in such scenarios.

In a recent example, Dewan Housing Finance Limited (DHFL) had raised close to 45,000 crores INR from investors through bonds and fixed deposits. They were supposed to use these funds to offer home loans to customers at a higher interest rate than the coupon rate of the bond and make the profit on the interest differential. However, allegations about the company owners later came to light - that they had redirected 33,000 crores INR into their personal pocket. The company then started defaulting on its interest payment to the bond holders.

The lenders, both the banks and bond holders reached out to the NCLT for repayment in 2019. NCLT stands for National Company Law Tribunal and is a special court responsible for settling such default or bankruptcy cases. Currently, the NCLT has invited bidders to buy out the business assets of the company: in this case home loans given out by DHFL (home loans given out by DHFL are assets on their balance sheet). Once the buyer and price are finalized, the company will be sold and the bondholders will be paid back.

However, it’s been 2 years of waiting for the bond holders and they are likely to get back only a small % of their money. This is because most of the money was siphoned off by DHFL’s founders which meant few home loans were given out. So the assets on their balance sheet are not enough to pay back the bonds.

Now, not every company runs a Ponzi scheme like DHFL’s scam with your money. But there is still some bit of credit risk associated with all the bonds. It can be high for some bonds and low for others depending on who is issuing the bond. So how do you know which bond is good and which one is bad before investing your hard-earned money in it?

Enter Credit Rating Agencies

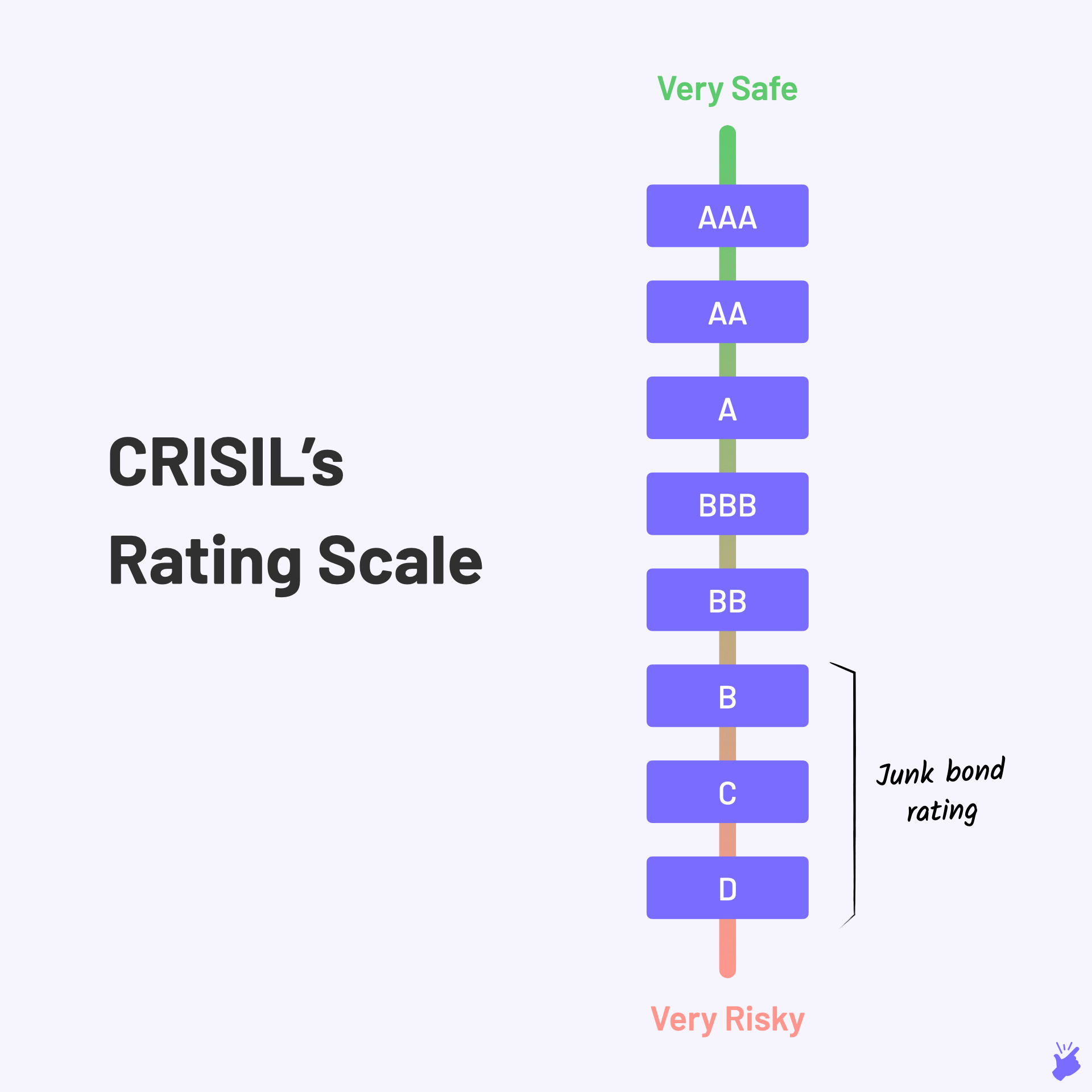

Just like individuals are assigned credit score basis their repayment history, companies raising debt are issued a credit rating too. CRISIL, ICRA and CARE are a few of the major credit rating agencies in India.

Rating agencies are independent entities that assess the creditworthiness of a bond by auditing the company issuing that bond. They do this by assigning a rating to the bond which conveys the probability of the money being paid back to the bondholder.

The rating scale used by CRISIL, one of the largest rating agencies in India, is shown below. AAA rating means the bond is extremely safe (very low chance of the company not paying back) and D rating means a high chance the company will not pay back the money. All bond issuing companies rely on credit ratings to signal their credibility to potential investors.

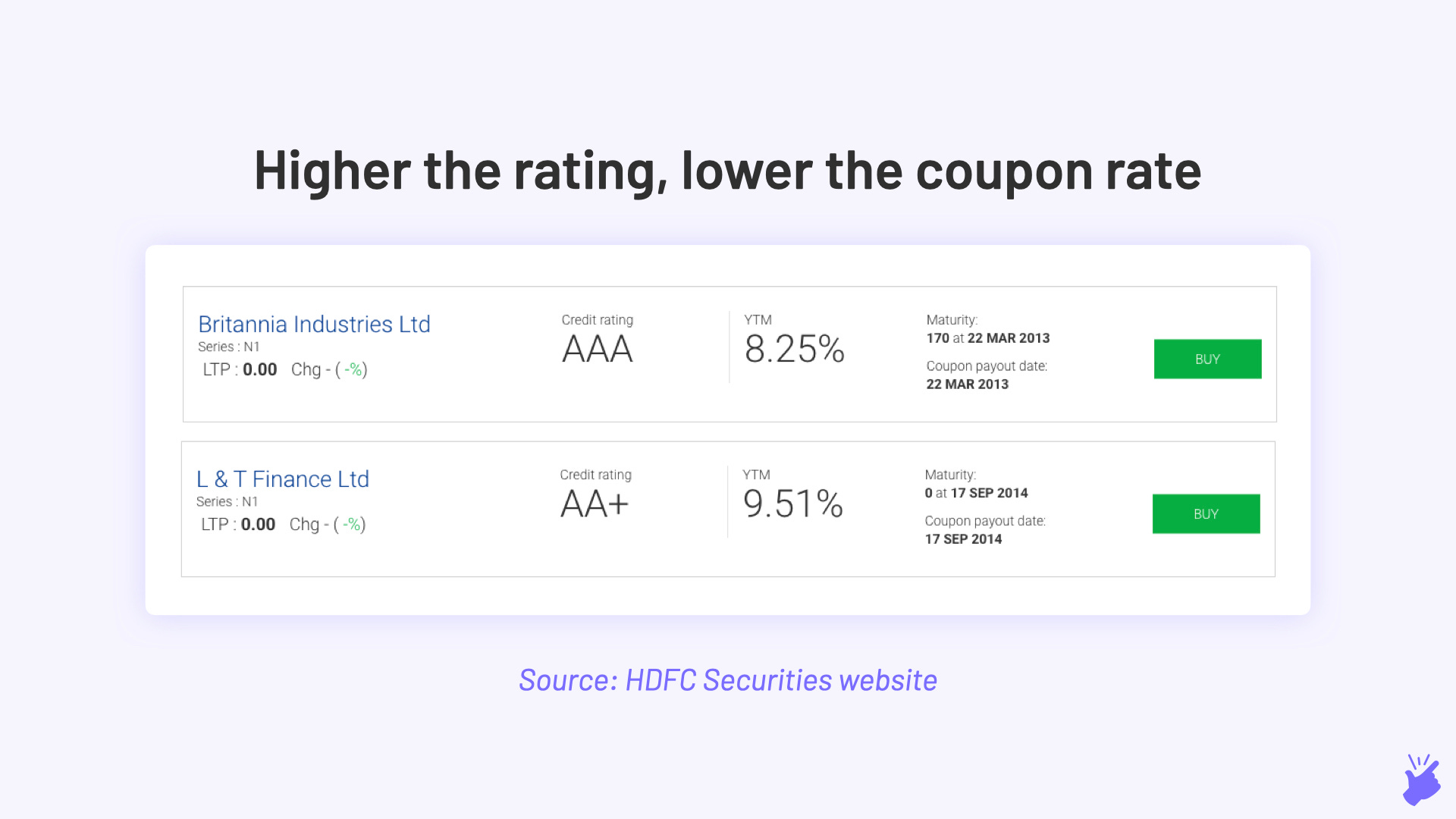

Most of the bonds issued by government agencies are rated as AAA and are considered to be the safest. The lower the rating of the bond, the higher the coupon rate the company needs to pay its investor. For instance, Power Finance Corporation, a public-sector company has an AAA-rated bond and hence can offer a lower coupon rate than L&T Finance which has an AA-rated bond. The difference in coupon rates is to account for the difference in risk.

Important note: Credit ratings do offer a certain level of safety to investors. But that doesn’t mean that they are completely accurate in all cases. Credit agencies can be wrong at times. Going back to our DHFL example, CARE maintained the highest rating of ‘AAA’ on DHFL’s bonds from 2016 till 2019. And in only a span of 3 months after DHFL started defaulting on its payments, they downgraded its rating to D. Ideally, the rating agencies should be smart enough to identify the possibility of a company defaulting on its payments before it actually happens.

In short, credit rating agencies do help you filter your choices and thereby reduce your credit risk but history has shown they are not 100% bankable.

Hmm...anything more I can do to reduce credit risk?

Yes. Investors have two other options to reduce credit risk in bond investments: Debt Mutual Funds and Covered bonds.

1. Debt Mutual Funds

Like any other mutual fund scheme, Debt Mutual Funds manage and invest client’s money in a portfolio of bonds. Debt mutual funds solve two problems for investors. Firstly, they help investors reduce credit risk by diversifying the investments across bonds of different companies. Secondly, they allow investors access to a lot of highly safe government, public-sector, and large corporate bonds which typically have a very high ticket size (minimum investment of INR 10,00,000).

Below is a snapshot of the holdings of one of the debt mutual fund schemes run by ICICI. As we just learnt, the investments are spread across multiple bonds. So even if this mutual fund had an allocation (say 2-4%) in a company like DHFL that defaulted, their returns would not be severely impacted. Also notice that a very high percentage has been invested in the government bonds (AAA rated). A lot of the government bonds mentioned here would have a minimum investment requirement of close to 10 lakhs INR. But debt mutual funds enable you to invest amounts as small as Rs.5000 into these safe bonds.

Important note: Whenever you are looking to invest in a debt fund, don’t look at the return of the fund alone. Instead, look at the bond holdings in their portfolio. A fund generating a high return can also mean they are investing in bonds with high coupon rates, ie, riskier bonds. This can mean a lot of trouble for the fund and you.

Take the case of Franklin Templeton fund house which had to close 6 of their debt mutual fund schemes last year. Franklin Templeton invested a good portion of their investments in lower-rated bonds (A and B rated bonds) from companies like ADAG (Anil Dhirubhai Ambani Group), Essel Group, and Vodafone India. They hoped that these higher risk bonds would deliver good returns. But when these companies ran into financial troubles and couldn’t pay the interest, Franklin Templeton and its investors lost money. Crores of it.

To conclude, investing in debt mutual funds is definitely less risky than investing individual bonds. But as the Franklin Templeton debacle shows, it still carries an amount, however small, of credit risk. But there is one more category of debt instruments called Covered Bonds which will safeguard your investment completely, even if the bond issuing company defaults. Thus eliminating credit risk entirely. The icing on the cake - it doesn’t even require the investors to wait for the NCLT to find buyers for collateral assets to get back the money. So how do these work?

2. Covered Bonds

Covered bonds have been in the west for a few decades now but gained popularity after the global financial crisis of 2008. The total covered bonds in circulation globally are $2.9 trillion (EUR 2.4 trillion). In India, covered bonds are a very recent phenomenon. In 2019, Kogta Financial India Limited, an NBFC, became the first Indian company to issue covered bonds. This was followed by a larger issue of 125 crores INR by another NBFC, Muthoot Finance, in 2020. These bonds are likely to become more popular in the coming times because they solve the credit risk problem - a problem plaguing the Indian bond markets currently.

Time to understand how these bonds solve credit risk.

Let's say there’s an NBFC “Hera Pheri Lending” (HPL) which gives home loans. HPL wants to raise 100 crores INR from investors via covered bonds. To do that, HPL needs to keep aside collateral (security) for these bonds. In this case, the collateral would be a pool of home loans issued by HPL in the past to its customers (as we learnt earlier, past loans given out by an NBFC are its assets because they generate regular income in the form of repayments).

Now, this is where the difference comes in. In the case of a traditional bond offering, the collateral (HPL’s home loans) will continue to remain on HPL’s balance sheet. But in the case of covered bond offering, HPL will first have to sell the collateral to another company. This company is newly formed specifically for the purpose of buying this collateral, meaning it is a Special Purpose Vehicle or “SPV”. This SPV is an independent body approved by the regulator (Securities and Exchange Board of India/SEBI) to act as a trustee of the collateral sold by HPL. So the collateral (HPL’s past loans) is no more on its balance sheet. Instead, it lies with the SPV whose ownership rights lie with the bond investors.

Suppose HPL goes bankrupt and cannot pay back the bond investors anymore, the bond investors have access to the collateral (HPL’s past home loans that are generating income) via the SPV. They don’t need to wait for the NCLT proceedings to get their investments back. Instead they earn from the repayments made on HPL’s loans that lie with the SPV, ie, HPL’s customers who are paying back their home loans. This extra protection is a unique feature of covered bonds and makes them much safer than traditional bonds. And since the risk of covered bonds is slightly lesser, the return they generate is also a little lesser (1-2% less) than the traditional bonds. And because of their safer nature, they get a higher rating from credit ratings agencies as well.

Important note: For covered bonds, the value of collateral to be kept with the SPV is typically 20-25% higher than the amount of bonds being issued. So HPL, which is raising 100 crores INR, has to sell 125 crores INR worth of home loans on its balance sheet to the SPV. This extra money provides a margin of safety for bond investors and increases the likeliness of them getting back their entire investment.

Another important note: Say HPL has issued 5-year bonds, ie, they will pay interest for 5 years and then pay back the entire amount. Over these 5 years, the value of collateral lying with the SPV will fall. This is because HPL’s home loan customers will continue repaying their loans (only the amount yet to be paid by a customer is an asset for the NBFC and this obviously decreases over time as customer repays). So the 125 crore INR collateral coils become 90 crore INR in 2 years time which is lesser than 100 crore INR of bonds that HPL issued. To account for this, HPL needs to keep adding to the SPV new home loans it gave out. They need to do this every month (or quarter) and ensure the value of the collateral lying with the SPV doesn’t fall below 125 crore INR. At the end of 5 years, once HPL has paid the 100 crore INR back to its bond investors, they can transfer the collateral from the SPV back to HPL’s balance sheet.

Phewww! This has become a really long post and I still need to cover a few more points. So there will be a sequel. In Part 2, we will explore strategies for investing in bonds, the impact of interest rates, and the term “yield”.

If you liked this piece, share it with your network :)

Thanks for the fantastic article. I have a doubt around HPL example. What if HPL went bankrupt and we are already seeing more defaulters on past loans that SPV has access to. In this case, will SPV have authority to liquidate the collateral or will investors have to reach out to NCLT for the same? Thanks for your time :)

This is a great article! Will wait for the Part 2.